As an incorporated physician, you face a unique set of financial planning questions. One of the most common is: “Where should I invest my money for the best long-term, tax-efficient growth?” Many doctors hear advice from colleagues to delay incorporating or to pull money out of their corporation to max out their personal TFSA and RRSP contributions first. While well-intentioned, this approach can be a significant drag on your wealth-building potential.

This guide will break down the roles of your corporation, TFSA, and RRSP, and outline a powerful hybrid strategy to optimize your financial future.

The Problem with the “TFSA/RRSP First” Approach

For a high-income professional, funding personal registered accounts from your corporation comes at a steep price. To contribute to a TFSA, you must first withdraw funds from your corporation as salary or dividends, paying personal income tax at your marginal rate. In provinces like Ontario, this rate can be as high as 53.53%.

This means to get $7,000 (the 2024 TFSA limit) into your account, you might need to withdraw over $14,000 from your corporation, with the other half going directly to taxes. This immediate tax hit significantly reduces the capital you have available to invest and grow.

Understanding Your Investment Vehicles

The key to effective planning is using each account for its intended purpose. Let’s compare the core mechanics.

The Professional Corporation: Your Primary Wealth Engine

Think of your corporation as the most powerful tool for long-term, inter-generational wealth building.

- The Power of Tax Deferral: You invest with corporate dollars that have been taxed at a much lower rate than your personal rate. This leaves a significantly larger sum of money to compound over time.

- Investment Flexibility: When you invest in growth-focused ETFs, the corporation can function like a super-charged savings vehicle. Tax on the investment income is paid at the corporate level, but you control when you realize the final layer of personal tax by choosing when to pay yourself dividends. This allows you to plan withdrawals for lower-income years, such as retirement, dramatically reducing your overall tax burden.

- Inter-generational Wealth Transfer: Unlike an RRSP, which is fully taxed upon the death of the second spouse, corporate shares can be passed to the next generation in a highly tax-efficient manner through strategies like an estate freeze.

The RRSP: A Strategic Retirement Piggy Bank

The RRSP is a valuable tool, but it should not be the sole focus of your accumulation strategy.

- Benefit: You receive a tax deduction for contributions, and the funds grow tax-deferred.

- Drawback: All withdrawals are 100% taxable as income. After age 71, you are forced to make minimum annual withdrawals from the converted RRIF, which can reduce or eliminate government benefits like Old Age Security (OAS) and create a significant tax liability in your later years and upon death

- Best Use: Use the RRSP as a supplementary retirement fund. Contribute enough to manage your current tax bracket, but avoid building an excessively large balance that will create a tax problem for you or your estate later.

The TFSA: Your Short-Term & Tactical Tool

The TFSA offers the incredible benefit of completely tax-free growth and withdrawals.

- Benefit: Unmatched for tax-free growth.

- Drawback: Must be funded with after-tax dollars, making it inefficient to fund with high-taxed corporate withdrawals.

- Best Use: Ideal for short-to-medium-term savings goals like renovations, a major vacation, or a wedding. It’s best funded during lower-income years (e.g., parental leave) or with funds paid to a lower-income spouse.

The Hybrid Strategy: A Framework for Success

A sophisticated financial plan doesn’t choose one vehicle; it integrates all three.

- Prioritize the Corporation for Long-Term Growth: The majority of your long-term investments, especially in growth-oriented equity ETFs, should be held within your corporation. This is your primary engine for building substantial, tax-efficient wealth.

- Build Your RRSP Strategically: Use your RRSP to fine-tune your annual tax bill, but don’t make maxing it out your primary goal. Plan for it to be a source of income in retirement, complementing your corporate funds.

- Use Your TFSA Tactically: Reserve the TFSA for upcoming life expenses and fund it when you can do so in a tax-efficient manner.

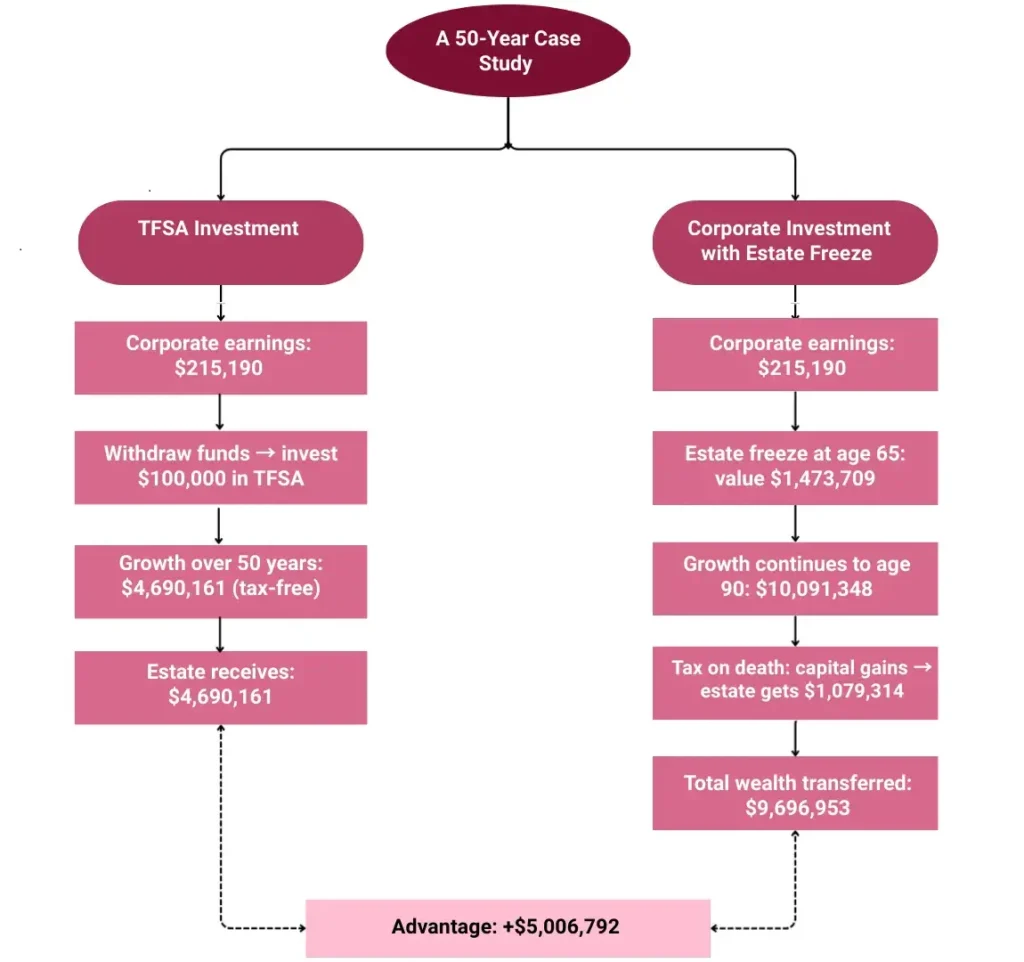

The Math: A 50-Year Case Study

Let’s compare the outcomes for a 40-year-old doctor who invests over a 50-year horizon, living to age 90.

Assumptions:

- Initial Capital: $215,190 of corporate earnings.

- Investment: A pure growth ETF with an 8% annual compounded return.

- Tax Rates: Top marginal rates for an Ontario resident (2025).

- Estate Plan: In the corporate scenario, an estate freeze is performed at age 65.

Scenario 1: TFSA Investment

To invest in a TFSA, the doctor must first pay personal tax on the corporate earnings.

- Initial Investment:

- Pre-Tax Corporate Earnings: $215,190

- Personal Tax Paid Upfront (53.53%): ($115,190)

- Net Amount Invested in TFSA: $100,000

- Investment Growth: The $100,000 grows entirely tax-free within the TFSA for 50 years.

- Value at Age 90: $100,000 x (1 + 8%)^50 = $4,690,161

- Taxes Upon Death: There are no taxes payable on a TFSA upon death.

- Net Worth to Estate: $4,690,161

- Total Tax Paid: $115,190 (paid in year 1)

Scenario 2: Corporate Investment with Estate Freeze

The corporation invests the full pre-tax amount, and an estate freeze at age 65 passes future growth to the next generation.

- Initial Investment: The corporation invests the full $215,190.

- Estate Freeze at Age 65: After 25 years, the investment is worth $1,473,709. An estate freeze is executed, capping the value of the doctor’s shares at this amount. New “growth” shares are issued to the children, who will receive all future growth.

- Taxes Upon Death at Age 90: Upon death, the doctor is deemed to have sold their shares for their “frozen” value, triggering a capital gain.

- Value of Shares at Death: $1,473,709

- Tax on Final Return (Capital Gains): $1,473,709 x 26.76% = $394,395

- Post-Mortem Planning: To avoid double taxation when the estate accesses the funds, a “pipeline strategy” is used. This complex strategy effectively allows the estate to receive the funds by only paying the initial capital gains tax.

- Net to Estate (from frozen value): $1,473,709 – $394,395 = $1,079,314

- Value Accruing to Children: The growth from age 65 to 90 belongs to the children.

- Total Corporate Value at Age 90: $10,091,348

- Value Frozen for Doctor: $1,473,709

- Value for Children (in corporation): $8,617,639

The Verdict: A Clear Winner for Generational Wealth

| Metric | TFSA Scenario | Corporate Scenario (Pipeline) |

|---|---|---|

| Net Value to Doctor’s Estate | $4,690,161 | $1,079,314 |

| Value to Children (in Corp) | $0 | $8,617,639 |

| Total Net Worth Transferred | $4,690,161 | $9,696,953 |

| Advantage of Corporate Strategy | +$5,006,792 |

The corporate strategy, combined with an estate freeze, results in over $5 million more in total wealth being transferred to the next generation. This is the power of tax deferral—investing the full, larger pre-tax amount allows for decades of supercharged compound growth that far outweighs the initial tax savings of the TFSA route.

For the incorporated physician, the path to optimal wealth creation is not about choosing one account over another, but about implementing a cohesive, hybrid strategy. By prioritizing your corporation as your primary long-term investment engine and using your RRSP and TFSA for their specific tactical advantages, you can build a more robust and tax-efficient financial future. Learn more about estate freezes and transferring future growth tax‑efficiently here.

Disclaimer: This post is for informational purposes only and does not constitute professional tax advice. Every individual’s financial situation is unique. Please consult with a qualified tax professional who specializes in serving incorporated physicians to develop a plan tailored to your specific circumstances and goals.

Take the first step toward success!

Ready to maximize your wealth through smart strategies? Discover how to invest effectively using your Corporation, TFSA, and RRSP. Schedule your free consultation today!